Lists are useful devices. Grocery lists help you remember to buy bread and milk. To-do lists keep you on point during your workday. These lists are used often enough that you practically have them memorized. That’s not the case with a list of items you need for tax preparation. Your accountant only asks for those once a year. That time has come.

You can download the list by submitting your name and email on our tax return preparation page, but we wanted to review it here, so you understand why we need the documents we’re requesting. Lists make more sense when you can internalize why we create them. In this case, we want to ensure you’re covered for any changes in the tax laws.

W2s, 1099s, and Payroll Deduction Statements

If you’re an employee, your company will send you a W2 form sometime in January. Many companies do this electronically now, so don’t wait by the mailbox. If you have a gambling income of over $600 from last year, you’ll receive a W2G. Make sure you have those in a folder with any other W2s when you come in for your tax prep appointment.

Self-employment is slightly different. Your clients must send you a 1099 if you’re an independent contractor. The due date for them to file those with the IRS is February 28th for paper forms and March 31st for electronic filing, but you’ll likely receive your copy sometime in January. If it comes in electronically, print a hard copy to put in your tax folder.

You may also receive a 1099 for your retirement fund and any investment funds you have. Put them into a folder with your other 1099s and W2s. Add any statements that detail contributions you made to your retirement account or payroll statements that show deductions for HSA/HRA/MSA accounts. Social security statements also fall in this category.

Income, Expenses, Capital Gains, and Losses

Gathering this paperwork is easier when you understand why it’s important. The IRS assesses taxes on income. Expenses, like the payroll deductions to your HSA account, lower your total income, thereby reducing your tax liability. A professional accountant knows which deductions to look for, so bring in all your payroll statements. We’ll sort them out for you.

Capital gains and losses are another important variable when calculating your tax liability. If you made a profit selling stock during the year, you have a “realized” gain. Just to clarify, a “profit” is defined as selling the stock for more than what you bought it for. The gain is “realized” because you sold it. An unsold stock that’s increased in value has an “unrealized” gain.

A realized gain counts as income, so it increases your tax liability. An unrealized gain does not. A loss, which is when you sell the stock for less than what you bought it for, can be used to lower your income. Ask us about this when you come in for your next visit. If you’re an active investor in the stock market, we should also talk about tax loss harvesting for next year.

The Tax Benefits of Homeownership

We published an article here last August that went over several tax deductions you may be eligible for if you’re a homeowner. The article is a listicle (of course) that’s titled, “7 Steps Homeowners Can Take Now to Prepare for Next Year’s Tax Filings.” If you read it back then, you may have already taken some of those steps. If not, you can check it out here.

The most common tax deduction homeowners take is the mortgage interest deduction. Your mortgage company should send you a statement that breaks down how much you paid in interest and how much you paid in principle. The interest is 100% tax deductible if the mortgage is on a primary or secondary residence. That can add up to a lot of money.

If you bought your house last year, you may also be able to deduct mortgage points. Ask us about this and other deductions, like the SALT Deduction for property taxes, interest deductions on HELOCs, or energy credits for green energy home improvements. Any combination of these could be possible, significantly reducing your tax liability.

Mileage Logs and Education Deductions

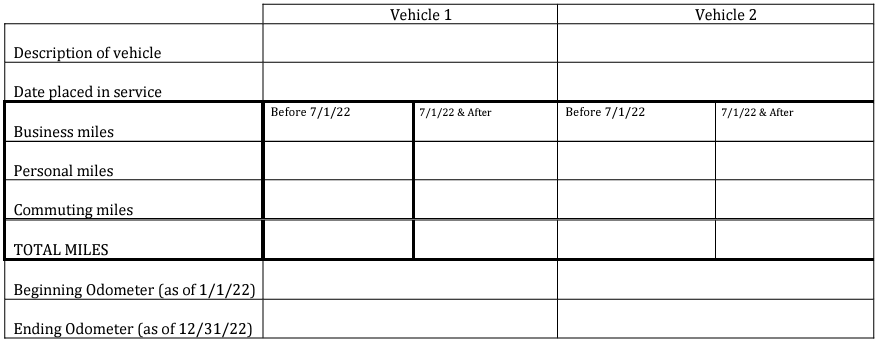

Self-employed individuals and owners of rental properties can deduct their mileage at the standard mileage rate of 67¢ per mile for the 2023 tax year. Your mileage log proves those miles were traveled for business purposes, so make sure you keep one. There’s also an actual expense method that can be used to deduct auto expenses. Ask us about that too.

Tuition for higher education may also be tax deductible, but some of the IRS rules on this have changed. The deduction is available for self-employed individuals putting themselves through school, but it may not be federally deductible for W2 employees. Some states offer deductions for tuition, including Wisconsin. You can read more about that at Wisconsin.gov.

There are several forms listed in our checklist that are relevant if you paid tuition last year. One is Form 1098T from your college, which is a statement of how much you paid in tuition and fees. You’ll need that, along with your 529 Plan year-end documents. If you made payments on student loans, add a 1098E statement to the folder.

Don’t Forget the Basics Go to our tax return preparation page again to download the full list of everything you need. You also don’t want to forget the basics. Those are last year’s tax return and a valid ID for you and your spouse. If we did your taxes last year, we have them in our files, but you should bring your copies anyway. Let’s get 2024 off on the right foot by doing your taxes early.